Foundation Insurance Coverage Checker

Check if your foundation damage is covered

Most building insurance policies don't cover foundation repair unless caused by a sudden, covered event. This tool helps you assess your coverage based on your situation.

Coverage Assessment

Most homeowners assume their building insurance covers everything that goes wrong with their house. But when a crack appears in the foundation or the basement walls start leaning, many are shocked to find out their claim got denied. The truth? Foundation repair is one of the most common claims that gets turned down - and not because the damage isn’t serious. It’s because most policies have clear, often hidden, exclusions.

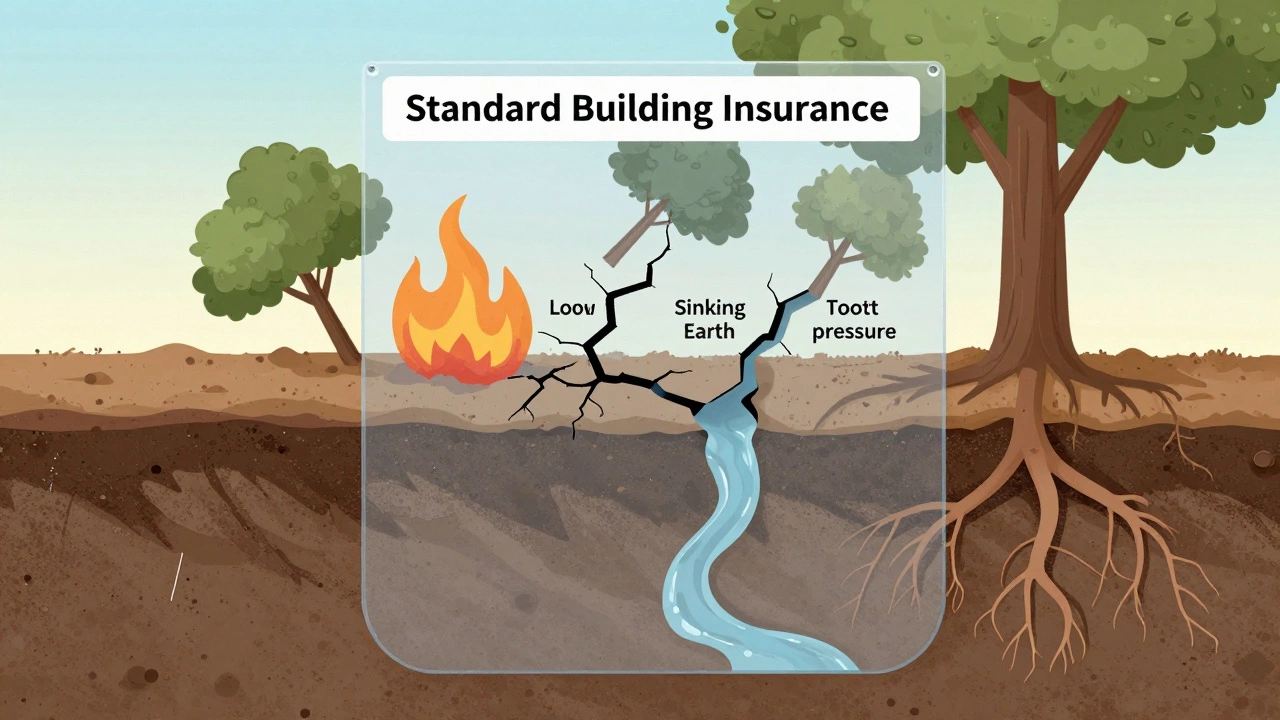

What Building Insurance Actually Covers

Building insurance typically protects against sudden, accidental damage from events like fires, storms, lightning, explosions, or falling trees. If a windstorm knocks your roof off, your insurance will likely pay to fix it. If a pipe bursts and floods your basement, that’s usually covered too. These are called “insured perils” - sudden events you couldn’t have prevented.But foundation problems? They rarely qualify. Most policies don’t cover damage that happens slowly over time. That’s the key difference: sudden vs. gradual.

What’s Usually Excluded? Foundation Damage

Here’s what most building insurance policies won’t pay for when it comes to your foundation:- Settling or sinking - Every house settles a little after construction. But if your foundation shifts over years due to soil compaction, your insurer won’t cover it. This is considered normal wear and tear.

- Soil expansion - Clay soils swell when wet and shrink when dry. This constant movement can crack foundations over time. Insurance sees this as predictable, not accidental.

- Poor drainage - If water pools around your foundation because your gutters are clogged or your yard slopes toward the house, repairs won’t be covered. You’re expected to maintain your property.

- Tree root damage - Roots from large trees near your home can push against foundations. Insurance treats this as a maintenance issue, not a covered peril.

- Old or deteriorating materials - If your foundation was built with weak concrete or outdated techniques, and it’s now cracking, that’s not covered. Insurance doesn’t replace aging infrastructure.

- Earthquakes and floods - These are almost always excluded unless you buy separate coverage. In Vancouver, where seismic activity is real, this is especially important.

Why Do Insurers Exclude These?

Insurance companies aren’t trying to be unfair. They’re protecting themselves from claims that are predictable, expensive, and often preventable. Foundation repair can cost $20,000 to $80,000 depending on the damage. If every homeowner filed for slow-moving foundation shifts, premiums would skyrocket.Think of it this way: your car insurance won’t cover engine wear from not changing the oil. Same logic applies to your home. If you ignore drainage, don’t fix gutters, or plant trees too close to the foundation, the damage is seen as your responsibility.

Real-Life Example: A Vancouver Homeowner’s Story

A homeowner in North Vancouver noticed a 1/4-inch crack in their basement wall in 2022. They thought it was minor and didn’t act. By 2025, the crack widened to 1.5 inches. The wall was leaning. A structural engineer said the foundation had shifted due to decades of moisture buildup from poor grading. The homeowner filed a claim - and got denied. The insurer’s report stated: “Damage resulted from gradual soil movement, not sudden event.”They ended up paying $47,000 out of pocket for underpinning and drainage correction. That’s not rare. In BC, nearly 60% of foundation claims are denied for reasons tied to gradual damage.

What You Can Do

Don’t wait until your walls are leaning. Here’s how to protect yourself:- Inspect annually - Look for cracks wider than 1/8 inch, doors that stick, or uneven floors. Take photos each year to track changes.

- Fix drainage - Make sure gutters are clean, downspouts extend at least 6 feet from the foundation, and your yard slopes away from the house.

- Monitor trees - Keep large trees at least 15 feet from your foundation. Roots can travel far and cause hidden damage.

- Consider a home warranty - Some home warranty plans cover foundation repair, especially if you have a service contract from your builder.

- Buy separate earthquake or flood insurance - In BC, these are not optional if you want real protection.

What About New Homes?

New construction comes with a builder’s warranty - usually 2 years for workmanship and up to 10 years for structural defects in BC. But this isn’t insurance. It’s a guarantee from the builder. If the builder goes out of business or refuses to honor the warranty, you’re stuck.That’s why some homeowners in Vancouver buy additional “latent defect insurance” - a policy that covers structural failures even after the builder’s warranty expires. It’s not cheap, but it’s a smart move if you’re in an area with reactive soils or high rainfall.

When Insurance Might Cover Foundation Repair

There are exceptions. If a covered event directly causes foundation damage, you might get paid. For example:- A tree falls on your house during a storm and crushes part of the foundation - covered.

- A burst water main under your yard causes sudden soil erosion - covered.

- A gas explosion damages your basement walls - covered.

In these cases, the foundation damage is a side effect of a covered peril. But if the damage happened before the event - or if the event just made existing damage worse - you’re still likely out of luck.

How to Check Your Policy

Don’t rely on what your agent told you. Read your policy. Look for these keywords:- “Gradual damage”

- “Settlement”

- “Earth movement”

- “Faulty workmanship”

- “Lack of maintenance”

If your policy says it excludes “damage resulting from earth movement or subsidence,” then foundation repair won’t be covered. Most standard policies in Canada include this language.

What to Do If Your Claim Is Denied

If you’ve been denied, don’t accept it without a second opinion. Hire an independent structural engineer to write a report. Sometimes, damage that looks like gradual settling is actually caused by a sudden event - like a broken water line under the slab. If the engineer can prove the damage started with a covered peril, you might reopen your claim.Also, check if you have a “law and ordinance” endorsement. In some cases, if your home was built before current codes and now needs upgrades to meet them after damage, that can be covered.

Final Thought

Building insurance is not a magic shield. It’s a safety net for disasters, not a maintenance plan. Foundation problems are silent, slow, and expensive. The best defense isn’t insurance - it’s awareness. Know your soil. Know your drainage. Know your limits.Don’t wait for a crack to become a chasm. Check your foundation now. Take photos. Fix what you can. And if you live in an area with clay soil, heavy rain, or seismic risk - talk to your insurer about what’s truly covered. You might be surprised.

Does building insurance cover foundation cracks?

Building insurance usually doesn’t cover foundation cracks unless they result from a sudden, covered event like a storm or explosion. Cracks from settling, soil movement, or poor drainage are considered gradual damage and are excluded from standard policies.

Can I get coverage for foundation repair through a home warranty?

Some home warranty plans do cover foundation repair, especially if the damage is linked to plumbing leaks or mechanical failures. However, most exclude damage from soil movement, tree roots, or long-term settling. Always read the fine print.

Is earthquake damage covered under standard building insurance?

No. Earthquake damage is almost always excluded from standard building insurance policies in Canada. You need to purchase a separate earthquake endorsement or policy, especially in regions like British Columbia where seismic risk is high.

What’s the difference between foundation repair and foundation replacement?

Foundation repair fixes cracks, leveling, or shifting without removing the existing structure - often using underpinning or epoxy injections. Foundation replacement means tearing out and rebuilding the entire foundation, which is far more expensive and rarely covered by insurance unless caused by a sudden covered event.

How much does foundation repair typically cost in British Columbia?

In British Columbia, foundation repair costs range from $15,000 to $80,000 depending on the extent of damage. Underpinning, drainage correction, and crack sealing are common fixes. Full replacement can exceed $100,000. Most homeowners pay out of pocket because insurance rarely covers it.